A Deep Look Under The Hood: Taking a Closer Glance At The Q4 GDP Report

U.S. GDP Rose 2.9% in the Fourth Quarter After a Year of High Inflation reflecting return to more normal pace of growth. Or at least that’s what people think…

Valentin

March 13, 2023

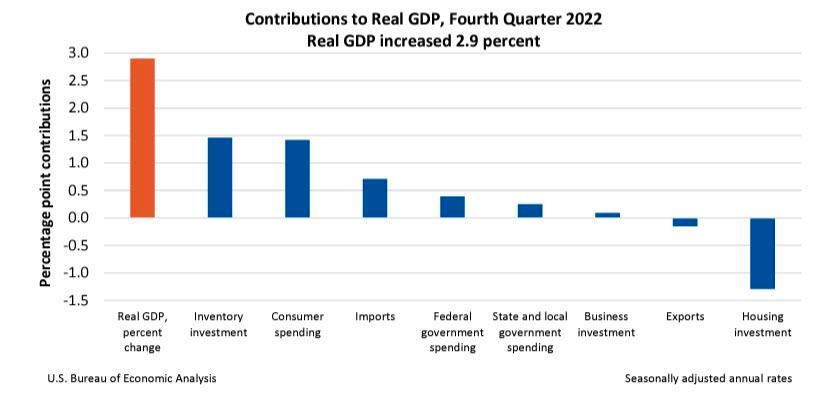

The Bureau of Economic Analysis (BEA) recently released its final estimate for Q4 GDP, which showed that US GDP rose by a stronger than expected 2.88%, a modest drop from the 3.2% in Q3 and well above consensus estimates of 2.6%

Real GDP in the fourth quarter increased due to growth in inventory investment, consumer spending, government spending, and business investment. However, this increase was partially offset by a decrease in housing investment and exports. Additionally, imports, which negatively impact GDP calculation, decreased.

Source: https://www.bea.gov/news/2023/gross-domestic-product

However, something to keep in mind is that although GDP growth exceeded expectations, private domestic demand was weak at 2.1%. This is likely to push back recession expectations to later in the year, with employment being the last metric to deteriorate.

The combined impact of household consumption, business investment and residential investment was just 0.22%, the weakest since Q2 of 2020. In contrast, inventories and exports contributed a combined 2.2%, which is the opposite of the trend seen in the first half of the year when strong demand was offset by other factors.

Furthermore, inventory reduction levels appear to have ended in Q3, and in Q4, inventories increased once again. This suggests that in Q1, inventories will decrease again, leading to a negative impact on GDP. Economists familiar with the matter predict that GDP may decline in the current quarter, partly due to the accumulation of inventories.

As CIBC economist Katherine Judge stated,

“With inventories now elevated across many industries, and consumers running through excess savings, we see the potential for a contraction in the economy in the first quarter as the impact of past rate hikes materializes more fully, and consistent with a tapering off of momentum in recent monthly indicators.”

Bottom line

The main takeaway regarding the strong GDP print is that as the inflationary trend continues to remain stickier than policymakers initially anticipated, the Fed’s determined battle against inflation will continue to cause turbulence among financial markets.

Ultimately, the Federal Reserve must decide whether to allow the ongoing, long-term inflation to harm many Americans or to prioritize restoring price stability and reducing demand, even if it means sacrificing economic growth and employment. From what we have discussed in previous articles, it appears that the Fed has chosen the latter approach.